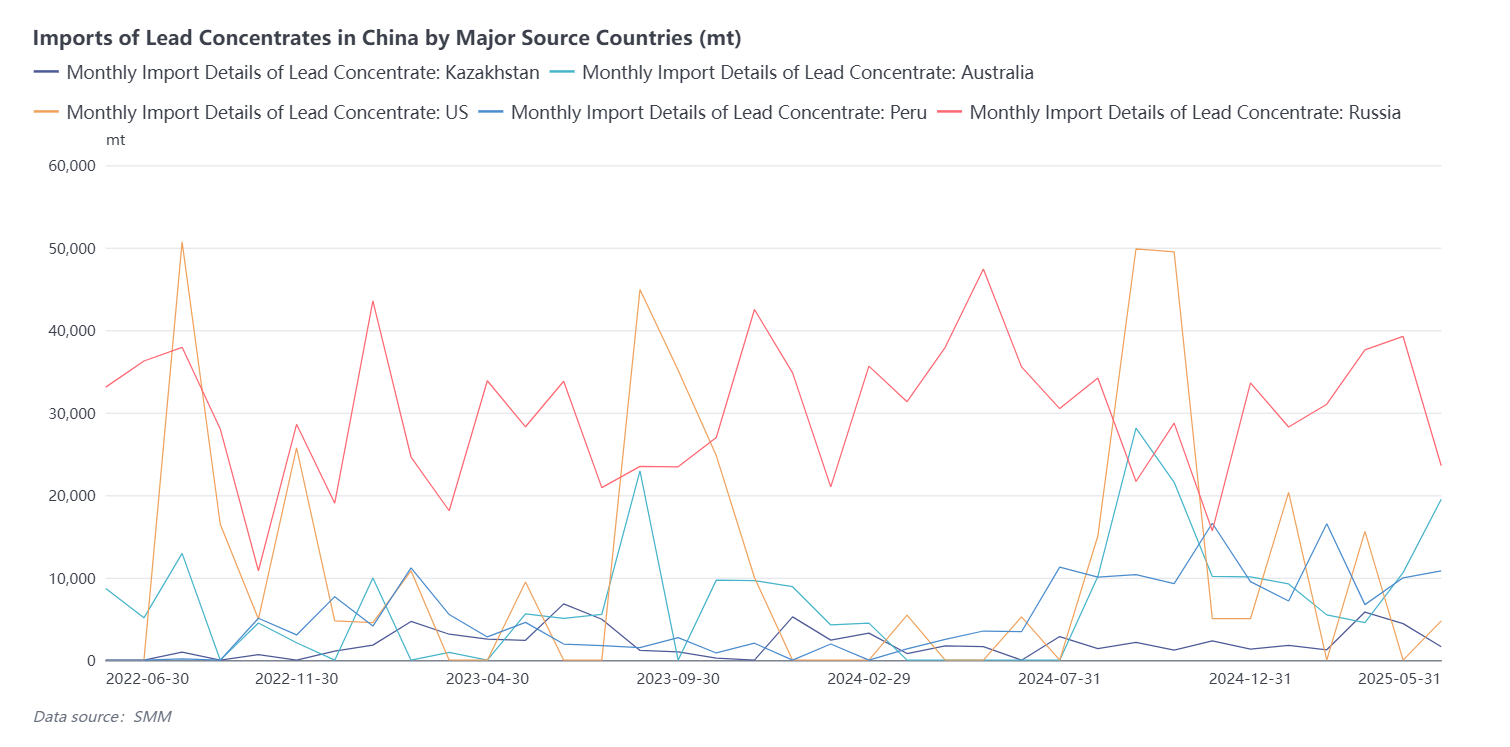

According to customs data, lead concentrate imports in May 2025 were approximately 104,000 mt, down 6.4% MoM but up 3.8% YoY. The cumulative imports for 2025 reached approximately 552,676 mt, marking a 64% increase YoY compared to 2024.

From the perspective of import profit margins, lead concentrate imports in May remained in a state of minor losses, with the import window yet to open. Additionally, in Q1, the supply of lead concentrates from regions such as Australia declined. Coupled with widespread market concerns about the prices of US Red Dog lead concentrates following the tariff hike in Q3, the tender and bid prices for lead concentrate TCs fell once again. Currently, imported lead concentrates still primarily rely on the trade market or long-term orders from smelters arriving at ports.

Despite lead concentrate imports increasing by over 60% YoY, silver prices continued to hit new highs in 2025, expanding the domestic and international arbitrage space and encouraging smelters to operate actively to achieve higher by-product revenues and export profits. Domestic lead concentrate supply remained relatively stable. However, due to factors such as the supply of imported ore falling short of expectations and the scarcity of high-grade ore, lead concentrate TCs fell again in June. According to smelters, the current quoted price for lead concentrates (pb50TC) with silver content ranging from 1.5-2 kg/mt is 0-200 yuan/mt (metal content), with additional payments for silver refining fees or coefficient pricing still required based on market conditions. Looking ahead to H2 2025, the outlook for lead concentrate imports remains pessimistic, and domestic lead concentrate supply is expected to continue in a state of tight balance.

Lead Concentrate Imports Continued to Decline in May 2025, with Lead Concentrate TCs More Likely to Fall Than Rise [SMM Analysis]

According to customs data, lead concentrate imports in May 2025 were approximately 104,000 mt, down 6.4% MoM but up 3.8% YoY. The cumulative imports for 2025 reached approximately 552,676 mt, marking a 64% increase YoY compared to 2024.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

![SMM April 2 Automotive Battery Market Summary [SMM Evening News]](https://imgqn.smm.cn/usercenter/msNEk20251217171722.jpg)

5 hours ago

SMM April 2 Automotive Battery Market Summary [SMM Evening News]

Read More

SMM April 2 Automotive Battery Market Summary [SMM Evening News]

5 hours ago

5 hours ago

LME Lifts Suspension on Umicore Lead Brands, to Be Rejected for Warranting from April 2026

Read More

LME Lifts Suspension on Umicore Lead Brands, to Be Rejected for Warranting from April 2026

[Developments in the Outside-China Lead Market] According to Notice No. 26,094-96 issued by the LME, the suspension of trading in the UMICORE 99.99, 99.985, and 99.97 lead brands produced by Umicore has been lifted, and these brands will continue to be used for warrant transactions on the London Metal Exchange (LME). It was reported that, according to Notice No. 26 005-007 issued by the LME on January 2, 2026, effective April 2, 2026, the three lead ingot brands produced by Umicore will no longer be accepted for warranting by the London Metal Exchange (LME).

5 hours ago

6 hours ago

Changan Automobile Rolls Out First Locally Made Vehicles in Brazil, Marking New Milestone in Sino-Brazil Cooperation

Read More

Changan Automobile Rolls Out First Locally Made Vehicles in Brazil, Marking New Milestone in Sino-Brazil Cooperation

[Automotive Market Updates] It was reported that on the highly automated production line jointly developed by Changan Automobile and its partner, the CAOA Group, the first batch of locally manufactured Changan vehicles in Brazil slowly rolled off the line. Recently, Changan Automobile's Brazil plant, located in Anápolis, Goiás, officially commenced production, marking a new milestone in China-Brazil industrial cooperation. In addition, Changan Automobile's products have entered 118 countries and regions worldwide, and the company has 76 factories outside China.

6 hours ago

Related News

SMM April 2 Automotive Battery Market Summary [SMM Evening News]

Apr 02, 2026 17:11

LME Lifts Suspension on Umicore Lead Brands, to Be Rejected for Warranting from April 2026

Apr 02, 2026 17:08

Changan Automobile Rolls Out First Locally Made Vehicles in Brazil, Marking New Milestone in Sino-Brazil Cooperation

Apr 02, 2026 16:24

Chinese E-bike Brands Plan Price Hikes of 200-300 Yuan Per Unit Starting April

Apr 02, 2026 16:15